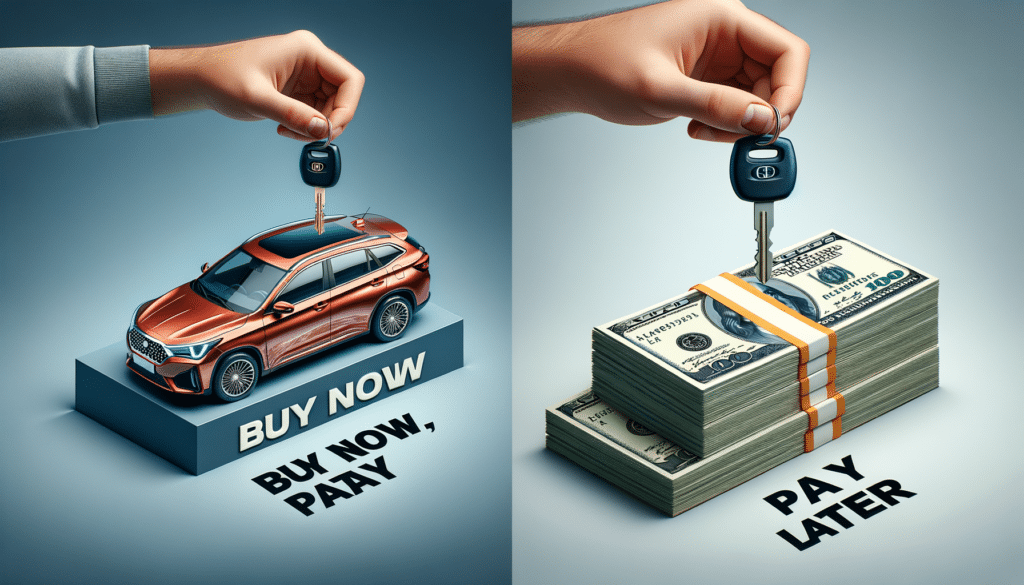

Understanding Buy Now, Pay Later for Cars

The “Buy Now, Pay Later” (BNPL) model has gained significant traction across various industries, including the automotive sector. This financing option allows consumers to acquire a vehicle without needing to pay the full price upfront. Instead, the cost is spread over an agreed period, making it easier for individuals to manage their finances while still enjoying the benefits of a new car. This model is particularly appealing to those who may not have the immediate funds or prefer to maintain liquidity for other investments or expenses.

One of the primary attractions of the BNPL scheme is its accessibility. Traditional car loans often require a good credit score and a lengthy approval process. In contrast, BNPL options can be more lenient, offering a viable alternative for those with less-than-perfect credit histories. This flexibility opens up car ownership to a broader audience, promoting inclusivity in the automotive market.

However, it’s essential to consider the terms and conditions associated with BNPL agreements. While they offer convenience, they may also come with higher interest rates compared to conventional loans. Consumers should carefully evaluate the total cost of the car, including any additional charges, to ensure they are making a financially sound decision. Transparency in terms and conditions is crucial in helping consumers make informed choices.

Comparing BNPL with Traditional Car Financing

When deciding between BNPL and traditional car financing, several factors come into play. Traditional car loans typically involve a down payment, followed by monthly installments over a set period. These loans are often secured against the car, meaning the vehicle can be repossessed if payments are missed. BNPL, on the other hand, might offer more flexible terms, with some providers not requiring an initial deposit.

Traditional financing options might offer lower interest rates, especially for those with excellent credit scores. This can make them more cost-effective in the long run. However, the rigorous credit checks and eligibility criteria can be a barrier for some potential buyers. BNPL can be a more accessible option, albeit potentially more expensive over time due to higher interest rates or fees.

It’s crucial for consumers to weigh the pros and cons of each option. For those who value immediate car ownership without a substantial upfront cost, BNPL might be attractive. Conversely, individuals looking for a more cost-effective long-term solution might prefer traditional financing, provided they meet the eligibility criteria.

Key Considerations for Consumers

Before opting for a BNPL option for purchasing a car, consumers should conduct thorough research and consider several key factors:

- Interest Rates: Compare the interest rates of BNPL options with traditional loans to understand the total cost over time.

- Repayment Terms: Review the repayment schedule to ensure it aligns with your financial situation and future income projections.

- Hidden Fees: Be aware of any additional charges, such as late payment fees or administrative costs, which can increase the overall expense.

- Credit Impact: Understand how choosing a BNPL option might affect your credit score and future borrowing capabilities.

By considering these factors, consumers can make informed decisions that align with their financial goals and lifestyle needs. It’s also advisable to seek professional financial advice to navigate the complexities of car financing effectively.